{kind=link}

In this post, we will discuss the monopolistic competition equilibrium. The following topics will be the focus of our discussion.

- How do you find the monopolistic competition equilibrium long run?

- What happens to monopolistic competition in the short run?

We discussed the definition and assumptions of monopolistic competition in the previous article. If you missed it, refer to the article below.

Monopolistic Competition Assumptions

Demand Curve for the Monopolistically Competitive Firm

Monopolistic competition is a type of competition that exists in between two extremes. Perfect competition and the monopoly.

A perfectly competitive firm’s demand curve is a horizontal line with infinite price elasticity. The demand curve of a monopoly firm is the demand curve for the industry, and it is downward sloping, indicating lower demand elasticity because there are no substitutes in the market.

The demand curve for a firm under monopolistic competition will be somewhere in between the demand curves of these two extreme market situations. Because it is a market model that stands between the two extremes of monopoly and perfect competition.

- The demand curve of a monopolistically competitive firm is not perfectly elastic since the products are not similar.

- However, because there are close substitutes in the market, the demand curve is not less elastic as in the monopoly.

- In most cases, a firm in monopolistic competition will have a downward sloping demand curve with higher elasticity than a monopoly firm.

- In other words, a monopolistically competitive firm’s demand curve is downward sloping and has the least slope.

- It is not exactly parallel to the horizontal axis, but it is close.

What might happen if one firm lowers its price?

If a firm reduces its price, it might increase sales proportionately more than the reduction in price. Other firms will not be forced to react since the particular firm is one among a large number of sellers in the group. And, also the risk of losing clients to those firms is minimal.

The decrease in their revenue as a result of the firm’s increased sales, which lowers the price, will be shared by the entire group. However, there is a limitation of reducing the price without facing the other firms’ reaction. If the firm reduces its price beyond this point, other firms will react, and the price reduction will be unprofitable for him.

In perfect competition, a firm can increase its price up to a certain point without losing all of its sales. If he increases his price above this point, he will lose all of his sales. As a result, there is a limit to how much he can increase or decrease his price.

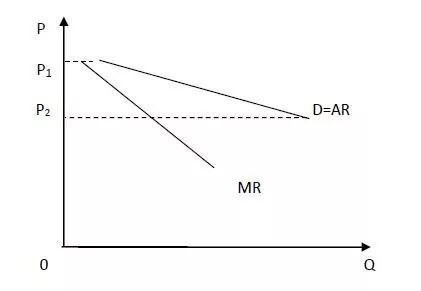

As seen in Fig. 1 below, under monopolistic competition, firms’ demand curves fall into a price range with the least slope:

You might find this explanation a little complicated. So let’s take a quick look at the most important points.

A firm under monopolistic competition can reduce its price without facing the reactions of the firms only up to a certain level.

When price reduction exceeds this level other firms will react against the price reduction, hence, the price reduction will not produce benefits to the group.

Hence, there is a limit that the price can be reduced.

Figure1: Demand curve of a firm under monopolistic competition

Short-run Equilibrium of a firm under monopolistic competition

We are going to discuss about the following points under this heading.

- How does a firm attain equilibrium in short run under monopolistic competition?

- What happens to monopolistic competition in the short run? (Profit or Loss)

In a monopolistically competitive market, the short-run equilibrium occurs when each firm’s plant size is fixed and the total number of firms in the market is also fixed.

However, analyzing the behavior of a monopolistically competitive firm is more difficult than analyzing the behavior of a perfectly competitive firm.

In addition to the price, the demand for the product of a firm is affected by the factors like advertisement, and other selling strategies. For the short-run equilibrium it is assumed that all such factors are being constant and price is the only relevant variable that affect the equilibrium.

Monopolistically competitive firm behaves as a monopoly firm in the short run because its product is different from other firms. Hence, he will follow the equilibrium conditions of the monopoly firm.

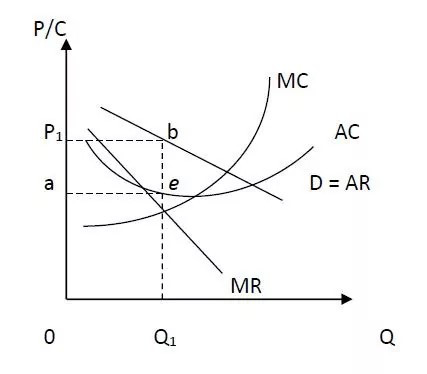

Accordingly, the necessary condition for the equilibrium is MR = MC and the slope of MR < slope of MC.

Figure 2: Short-run Equilibrium of a Firm

Equilibrium is at point e. At this point MR=MC and MC goes through the minimum point of the AC and at this point, slope of MC > slope of AC.

- Equilibrium price is P1

- Quantity is Q1

- TR = 0P1bQ1

- TC = 0aeQ1

- Supernormal Profit = aP1be

This indicates that monopolistically competitive firms can earn supernormal profit in the short-run.

Long-run Equilibrium of a Firm under monopolistic competition

Firms’ supernormal profits in the short run will encourage other firms to enter in the long run.

As a result, the supply of the group increases, and the market share of individual firms will decline.

So, the demand curve of the firms will shift down, implying that each firm can sell less quantity at every price than he sold in the short run.

In the long-run the average and marginal cost curves will shifts but for the simplicity we assume that they remain unchanged.

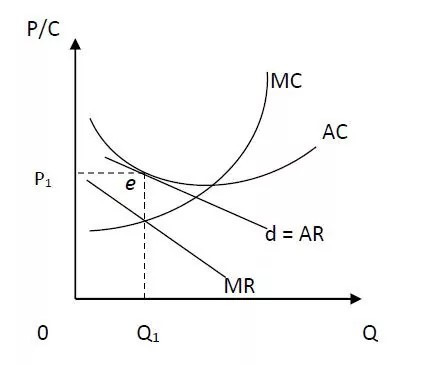

The firm will be in equilibrium when it earns just normal profit. To reach to the equilibrium by earning normal profit, the firms demand curve must be tangent to the falling part of the AC curve as shown in the Fig. 3.

Figure 3: Long-run Equilibrium of a Firm

The equilibrium conditions are satisfied at point e. At this equality of MC=MR, AC=AR but P>MC.

- Equilibrium price is P1

- The quantity is Q1

- Total revenue of the firm equals to the area of 0P1eQ1

- Total cost equals to the same area

In the long run, the firm generates a normal profit. In the long run, there is no tendency for firms to join or leave the group because they are all making normal profits.

In general, firms charge different costs, and certain brands may stand out more than others. Firms charge slightly different pricing in this case, and some will make a small profit.

Further Reading

Perfect Competition: Definition, Graphs, short run, long run

Top 5 characteristics of an oligopoly

Monopoly – Price discrimination: Types, Degrees, Graphs, Examples

Different Types of Monopolies| 7 Types

Monopolistic Competition and Economic Efficiency

Perfect Competition: Definition, Graphs, short run, long run

Monopolistic Competition Assumptions [Updated]

In this article we have discussed monopolistic competition equilibrium. We discussed the following points in relation to this topic:

Monopolistic Competition Equilibrium

Demand Curve of a Firm

Short-run Equilibrium of a Firm

Long-run Equilibrium of a Firm

Monopolistic Competition and Economic Efficiency will be discussed in the next article. [Updated]

In either case, I’d be delighted to hear from you. So please share your ideas in the comments section below.