{kind=link}

Perfect Competition market structure has a few necessary conditions that must be met. Before you know it, you need to know the basic features of a market.

So Let’s see the basic features of a market.

- Number of firms in the market

- Homogeneity of product

- It is difficult for new institutions to enter the market and for existing firms to leave the market

- Competition among firms in the market

Based on the changes in the above market characteristics, the nature of the market structures will also change. According to these criteria, we can easily identify four key market structures. Those are,

- Perfect Competition

- Monopoly

- Monopolistic Competition

- oligopoly

Now firstly let’s look at the conditions that a perfect competitive market must meet.

What Is Perfect Competition?

An industry or market is said to be operating under perfect competition if the following conditions are satisfied:

1. There are a large number of sellers/firms inside the industry.

The quantity supplied by each firm or seller is too small compared with the size of the market. Therefore, a single firm will not have any perceptible influence on the market price of the commodity and for the market supply. The firms are known as ‘price takers.’ They accept the price decided by the market.

2. There are a large number of buyers in the commodity market.

As for the sellers, buyers also cannot make any significant influence on the market price by their individual decisions. Hence they are also the ‘price takers’ in the market.

3. All firms are producing a similar product.

In other words, the products in the industry are homogeneous. The technical characteristics of the products and the services associate with its sale and delivery are identical. So this condition shows that buyers are indifferent in choice of the sellers from whom they buy it.

Because of the above assumptions on a large number of sellers and buyers and product homogeneity, individual firm or seller is a ‘price taker.’ The price of the commodity determines exogenously.

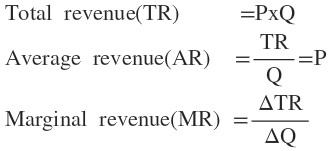

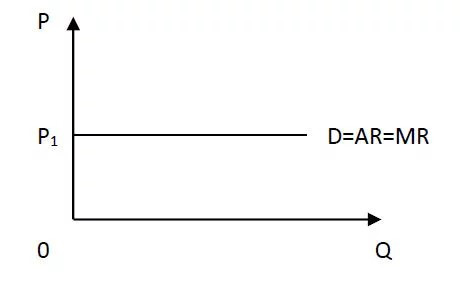

This implies that the demand curve of a firm is infinitely elastic (parallel to the horizontal axis). Indicating that the firm can sell any amount of output at the prevailing market Firm’s total revenue (TR) increases proportionately with its sales. Therefore, the demand curve of the individual firm is also its average revenue (AR) and its marginal revenue (MR) curves.

The market demand curve is given by the horizontal summation of the demand curves of individual firms. The total demand of the market is the sum of the quantity demanded by individual buyers. It is a straight line with a negative slope.

4. Free entry and exit.

The sellers are free to enter into the industry and leave the industry if it is not favorable, without any condition. So there will be no licensing, no control, and no government interference in the market.

5. Buyers and sellers have perfect knowledge of the market.

Both buyers and sellers have full knowledge about the quality of the product and its nature, price, and other attributes. There are no advertisement or other sales promotion activities.

6. There is no collusion among the buyers or sellers or sellers and buyers.

The trade and manufacturing associations, as well as consumer associations, do not exist in the market. Each customer and each seller is independent in making decisions.

When only the first four conditions are satisfied, then the market is said to be operated under ‘pure competition.’ So if all conditions are satisfied market operates under ‘perfect competition.’

The careful observation of the conditions of the perfect competition shows that it is more or less a hypothetical market situation.

It is extremely difficult to satisfy all these conditions. Despite this, we study this type of industries in economic theory, mainly because of the following reasons:

It provides,

- A simplified model to understand the complex economic system.

- Crude and approximate estimates of economic variables.

- A strong base for political ideology and welfare maximization.

- It helps in developing norms for desirable performance applicable to industry.

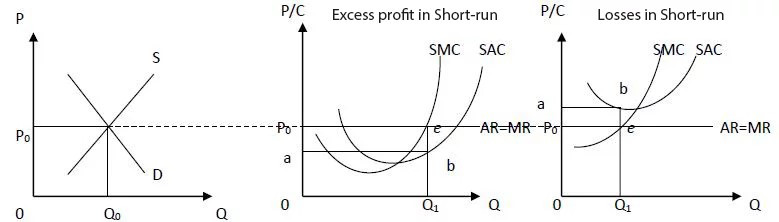

Short-run Equilibrium of the Firm: Graphical Analysis

Below graph shows the Short-run Equilibrium of the Firm.

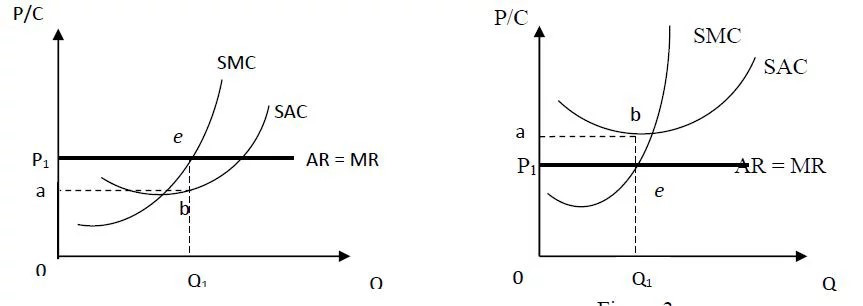

In the short, the firm is in equilibrium at point e. At this point,

MR=MC

MR= MC as the first-order condition. At this point, the second-order condition is also satisfied. That is, at point e slope of the MC curve is greater than the slope of the MR curve.

The slope of the MC > Slope of the MR curve

Since MC is always positive, at equilibrium MR also positive. The equilibrium price is P1 and the quantity is Q1.

What happens in the short-run perfect competition?

The total revenue of the firm is equal to the area of 0P1eQ1 and the total cost is equal to the area of 0abQ1. The revenue of the firm is higher than the cost. Hence, the profit of the firm equal to the area of P1eba. It is an excess profit or profit larger than normal profit.

The total revenue of the firm= 0P1eQ1

Total cost= 0abQ1

Profit of the firm= P1eba

This implies that in the short-run, a perfectly competitive firm can make an excess profit. However, it does not mean that the firms necessarily earn excess profit in the short-run. It depends on the level of the SAC (short-run average cost) in the short-run equilibrium.

If the SAC is below the price at the equilibrium, the firm earns an excess profit. But, if the SAC is higher than the price at the equilibrium, the firm makes losses.

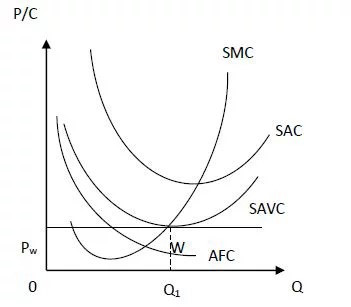

Producing with losses in the short-run perfect competition

Although the firm makes a loss in the short-run it will continue to produce. However, if it cannot cover its variable cost the firm will close down since by closing down the firm is better off. The point at which the firm covers its variable cost is called ‘the closing down point’. The closing down point is denoted by point w.

If the price falls below the Pw, (this price is equal to the minimum variable cost) the firm cannot cover all its variable cost, and hence, it will close down whereby minimizing the losses.

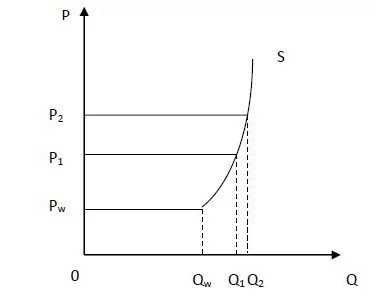

Supply Curve of the Firm and Industry

The supply curve of the firm can derive associate with the MC curve and demand curve of the firm. When the market price increases gradually it causes an upward shift in the demand curve of the firm. Since the firm’s demand curve is the MR curve, the firm reaches the equilibrium at the points where the successive demand curve cuts the MC curve.

The quantity supplied by the firm increases as price rises. If the price falls below Pw, the firm will not supply any quantity. The firm will close down when the price falls Pw.

If we transfer the successive points of interaction of the MC curve and the demand curves to the separate graph, the supply curve of the firm can be formed which is identical to its MC curve to the right of the closing down point ‘w’.

The supply curve of the industry is the horizontal sum of the supply curves of individual firms. The total market supply at each price is the sum of the quantities supplied by each firm at that price.

Short-run Equilibrium of the Industry

Given the market demand and supply, the industry is in equilibrium at the price that ‘clears the market’. At that price, market demand is equal to the market supply. As shown in figure equilibrium price and quantity are P0 and Q0, respectively. This will be a short-run equilibrium.

Under the prevailing market price, the firms can make excess profit or losses. So the firms that make losses in the short-run will make necessary adjustments. Otherwise, they will close down the firm in the long-run. The firms that earn excess profit will expand the size of the firms to maximize their profit.

Long-run equilibrium in perfect competition

In the long-run, firms can make the necessary adjustment to their capacity. Accordingly, they will adjust their capacity to produce at the minimum point of the long-run average cost (LAC) curve, which is tangent to the demand curve defined by the market price. In the long-run equilibrium, firms will earn just a normal profit which includes in the LAC (long average cost).

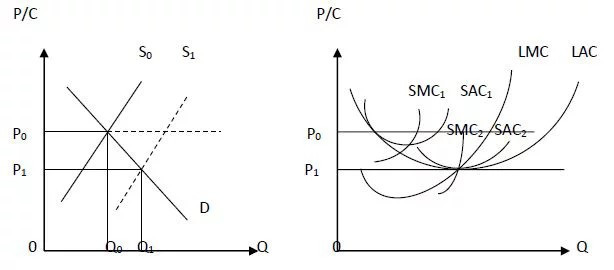

What happens in the long-run perfect competition?

If the existing firms are making an excess profit, new firms will enter the industry. Then the market price will fall down due to the increase of market supply with the new entrants’ supply. This will lead to shifting the demand curve down. Simultaneously, the cost curves will shift upward due to an increase in factor prices. These changes will continue until the LAC is tangent to the demand curve.

If the firms make losses inside the long-run they may go away the industry. As a result, the price will rise and the demand curve will shift upward. The cost will go down and price curves shift downward. These changes will continue until the remaining corporations attain the minimum factor of the LAC curve.

The below graph shows the firm which earns excess profits.

In the long-run equilibrium, firms adjust their capacity to produce at the minimum point of LAC, given the technology and factor prices.

At the equilibrium, SMC = LMC = LAC = P = MR

In the long-run equilibrium, both short-run and long-run equilibrium conditions coincide. When satisfying this condition the firm is working it’s optimal and no excess capacity and the resources are fully utilizing.

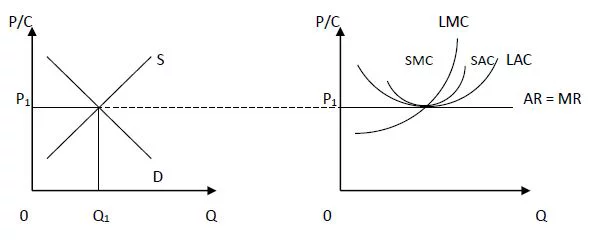

Long-run Equilibrium of the Industry

In the long-run, industry is in equilibrium when there is no tendency to expansion or contraction. So all the firms should be earned just a normal profit. In this situation, all firms will be operating at the minimum point of the LAC curve.

At the market price P1, firms are producing at their minimum cost, earning just normal profit. Hence there is no further entry to or exit from the industry. At the equilibrium point,

LMC = SMC = MR = P. This equality ensures that the firm maximize its profit.

Economic efficiency and perfect competition

Perfect competition is regarded as an ideal market situation. It believes that social welfare maximizes the long-run equilibrium under this market structure. In other words, economic efficiency can be achieved in the long-run equilibrium.

There are two different ideas of economic efficiency.

- The production of a commodity with the least cost (possible) combination of resources.

- In broader terms, resource allocation among commodities and therefore the composition of product mix in accordance with the preferences of the consumers and maximizes their satisfaction. In this sense, economic efficiency referred to as allocative efficiency.

Different ideas of economic efficiency

Long-run equilibrium under perfect competition achieves both the types of economic efficiency. In the long-run equilibrium

P=AC

So that no economic profits or losses are made by the firm.

Further, at the equilibrium P=MC and MC=LAC. This can happen only at the minimum point of the LAC. These ensure that firms are working at the minimum possible LAC. Working at the minimum point of LAC indicates that the firm utilizes its plants at full capacity.

These imply that economic efficiency in terms of the least-cost combination of resources can be achieved in the long-run equilibrium under perfect competition.

The second notion of economic efficiency defined as the allocation of resources in order to maximize the satisfaction of consumers also can be achieved.

Consumer satisfaction would be maximized when the marginal cost of production of a commodity equals the marginal utility which consumer derives from consuming a commodity. The price of a commodity can be interpreted as the marginal utility which indicates the willingness to pay.

If the level of supply falls short of equality, it implies that some units of the good are not producing which affects to increase the welfare of the society. Thus, maximum welfare is achieved if the production of the commodity is expanded to the level of equality point of MC with Price.

Questions

1. What are the characteristics of perfect competition?

2. What is a perfect competition in economics?

3. What is short run equilibrium under perfect competition?

4. What happens in the long-run perfect competition?

5. What is more efficient perfect competition or monopoly?

Conclusion

All right then. I really hope you learned this article.

Have you a question about something that I covered.

Either way, I’d like to hear from you. So go ahead and leave a comment below.

Related Articles

Short run equilibrium in monopoly

Perfect Competition: Definition, Graphs, short run, long run

Top 5 characteristics of an oligopoly

Monopoly – Price discrimination: Types, Degrees, Graphs, Examples

Different Types of Monopolies| 7 Types

Monopolistic competition assumptions

Monopolistic Competition Equilibrium| Long-run| Short-run

Monopolistic Competition and Economic Efficiency